Small Business Lending in 2026: Accessing Capital with Average Rates of 7%

Small business lending in 2026 is characterized by an average interest rate of 7%, necessitating that entrepreneurs understand evolving market conditions and diverse financing mechanisms to secure essential capital for growth.

As we approach 2026, the landscape for small business financing continues to evolve, presenting both opportunities and challenges for entrepreneurs seeking capital. Understanding small business lending in 2026 is crucial for any enterprise aiming to grow, innovate, or simply sustain operations in an increasingly competitive market. With average interest rates projected around 7%, knowing where to look and how to prepare can make all the difference in securing the funding your business needs to thrive.

The Current State of Small Business Lending in 2026

In 2026, the small business lending environment is shaped by a confluence of economic factors, technological advancements, and shifting regulatory landscapes. Businesses are navigating a market where traditional banks still play a significant role, but online lenders and alternative financing options are gaining substantial traction. The average interest rate of 7% serves as a benchmark, but actual rates can vary widely depending on the lender, the business’s creditworthiness, and the type of loan.

Economic stability, while generally improving, remains a key determinant. Inflationary pressures and central bank policies continue to influence the cost of borrowing. Small businesses must therefore remain agile, adapting their financial strategies to these broader economic currents. Access to capital is not just about securing funds, but about securing them at terms that support sustainable growth without overburdening the business with excessive debt.

Key Economic Factors Influencing Rates

Several macroeconomic indicators directly impact interest rates for small business loans. Federal Reserve policies, including benchmark interest rate adjustments, ripple through the entire financial system. Global economic stability, trade policies, and even geopolitical events can introduce volatility, affecting lender confidence and, consequently, lending terms.

- Inflation Rates: Higher inflation often leads to increased interest rates as lenders seek to protect the real value of their returns.

- Job Growth Data: Strong employment figures typically signal a healthy economy, which can encourage more aggressive lending practices.

- Consumer Spending: Robust consumer demand can boost business revenues, making them more attractive to lenders.

Understanding these underlying economic forces allows business owners to anticipate potential changes in the lending market, enabling proactive decision-making. By monitoring these indicators, businesses can better time their loan applications and negotiate more favorable terms, ensuring they are well-positioned for future financial endeavors.

Overall, the current state of small business lending in 2026 demands a sophisticated understanding of both micro and macroeconomic factors. Businesses that stay informed and adapt their strategies will be better equipped to secure the necessary capital at competitive rates. The 7% average interest rate is a guidepost, but the real challenge lies in navigating the complexities that determine individual loan terms.

Navigating Diverse Financing Options for Your Business

The array of financing options available to small businesses in 2026 is broader than ever, extending beyond traditional bank loans to include a variety of alternative and specialized funding sources. Each option comes with its own set of eligibility requirements, repayment structures, and, importantly, interest rates. Understanding these differences is crucial for selecting the most suitable path for your business needs.

From government-backed programs to private equity and crowdfunding, entrepreneurs have more tools at their disposal to secure capital. The key is to match the right financing type with your business’s stage, industry, and financial health. This strategic approach can significantly impact the long-term success and sustainability of your venture, especially when considering the average 7% interest rate environment.

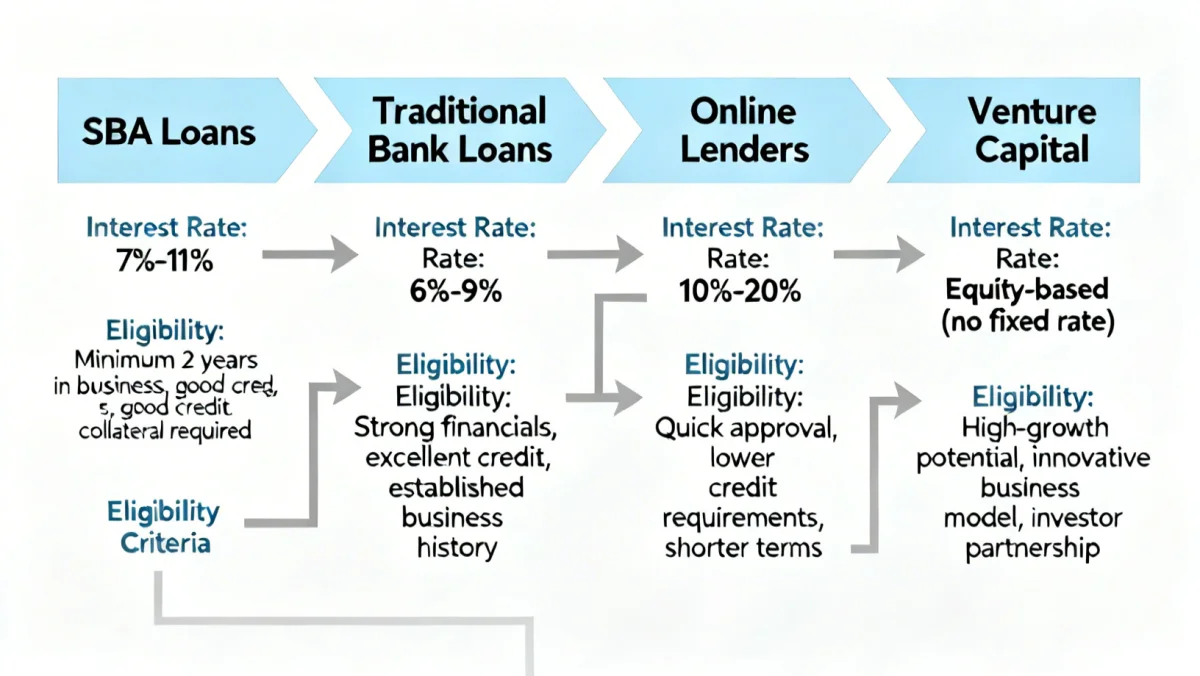

Traditional Bank Loans vs. Online Lenders

Traditional banks remain a cornerstone of small business lending, offering competitive rates and often larger loan amounts for established businesses with strong credit histories. Their rigorous application processes and longer approval times can be a deterrent for some, but the stability and often lower interest rates can be a significant advantage.

Online lenders, on the other hand, have revolutionized access to capital with their streamlined application processes and faster approval times. They often cater to businesses that might not qualify for traditional bank loans, or those needing quick access to funds. However, these conveniences often come with higher interest rates, which can sometimes exceed the 7% average, depending on the risk assessment.

- Traditional Banks: Generally offer lower interest rates, longer repayment terms, and larger loan amounts. Ideal for well-established businesses with strong financials.

- Online Lenders: Provide quicker access to funds, simpler application processes, and are more flexible with eligibility. Suited for businesses needing speed or those with less-than-perfect credit.

- Credit Unions: Often offer more personalized service and potentially lower rates than large banks, especially for members.

Choosing between these options requires a careful evaluation of your business’s immediate and long-term financial needs, as well as your capacity for repayment. The decision should not solely rest on the interest rate but also on the overall terms, flexibility, and the lender’s reputation. A comprehensive understanding of each option ensures a well-informed decision.

Successfully navigating the diverse financing landscape in 2026 means knowing your business’s financial requirements and aligning them with the most appropriate lending product. This strategic alignment is paramount to securing capital under favorable terms and fostering sustainable growth. The chosen financing route should support, rather than hinder, your business’s objectives.

Understanding the Average 7% Interest Rate and Its Implications

The average 7% interest rate for small business lending in 2026 is a crucial figure that businesses must understand. This rate is not a fixed universal standard but rather an aggregate reflecting various market dynamics, lender risk assessments, and loan types. Its implications extend beyond the simple cost of borrowing, influencing cash flow, profitability, and overall financial planning for small enterprises.

For many businesses, a 7% interest rate can be manageable, especially if the funds are used for growth initiatives that generate a higher return. However, it also means that businesses must carefully evaluate their return on investment for any project funded by borrowed capital. This benchmark rate necessitates a diligent approach to financial forecasting and budgeting to ensure that debt obligations can be met comfortably.

Factors Influencing Your Specific Interest Rate

While 7% is an average, your business’s specific interest rate will be determined by several factors unique to your situation. Lenders assess risk based on a comprehensive review of your business’s financial health, operational history, and the industry in which you operate. A strong financial profile can often result in rates below the average, whereas perceived higher risk might lead to rates significantly above it.

- Credit Score: Both personal and business credit scores are paramount. A higher score indicates lower risk.

- Business Longevity: Established businesses with a proven track record are generally viewed as less risky than startups.

- Revenue and Cash Flow: Consistent and strong revenue, along with healthy cash flow, demonstrates the ability to repay the loan.

- Collateral: Assets offered as security can reduce lender risk, potentially leading to lower interest rates.

Understanding these influencing factors allows business owners to take proactive steps to improve their financial standing before applying for a loan. This preparation can involve improving credit scores, strengthening financial statements, or even exploring options to provide collateral, all of which can contribute to securing a more favorable interest rate.

The 7% average interest rate in 2026 serves as a critical indicator, urging small businesses to not only seek capital but to do so with a clear understanding of how their unique circumstances will affect their borrowing costs. Strategic financial management and thorough preparation are key to optimizing loan terms and ensuring the long-term financial health of the business.

Strategies for Successful Capital Access in 2026

Accessing capital successfully in 2026, particularly with an average interest rate of 7%, requires more than just filling out a loan application. It demands a strategic and well-thought-out approach that addresses both your business’s needs and the lender’s requirements. Preparing thoroughly, understanding your financial position, and knowing how to present your business effectively are paramount to securing favorable terms.

The competitive lending environment means that businesses need to stand out. This often involves demonstrating a clear growth plan, a strong understanding of market dynamics, and a robust financial history. Proactive engagement with potential lenders and a willingness to explore various funding avenues will significantly improve your chances of success.

Preparing Your Business for Loan Applications

Before approaching any lender, it is essential to have your business in the best possible financial shape. This preparation involves meticulous record-keeping, a clear business plan, and a thorough understanding of your credit profile. Lenders look for stability, profitability, and a clear path to repayment, so presenting these aspects effectively is vital.

- Develop a Robust Business Plan: Outline your business model, market analysis, financial projections, and how the loan will be utilized for growth.

- Maintain Strong Financial Records: Keep up-to-date balance sheets, income statements, and cash flow projections. Lenders want to see a clear financial history.

- Improve Credit Scores: Work on both personal and business credit scores. Pay bills on time, reduce debt, and monitor your reports for inaccuracies.

- Gather Supporting Documentation: Have tax returns, bank statements, legal documents, and any existing contracts readily available.

A well-prepared application package not only expedites the lending process but also signals to lenders that you are a serious and responsible borrower. This can lead to better negotiation power and potentially lower interest rates, even in a 7% average rate environment. Investing time in preparation can yield significant returns in terms of funding access and cost.

Ultimately, successful capital access in 2026 hinges on strategic planning and meticulous execution. By proactively preparing your business and understanding the nuances of the lending market, you can position yourself to secure the necessary funding on terms that support your long-term growth and financial stability. This proactive stance is a hallmark of successful entrepreneurship.

The Role of SBA Loans and Government Programs in 2026

In 2026, Small Business Administration (SBA) loans continue to be a cornerstone for many small businesses seeking capital, especially those that might find it challenging to secure traditional financing. These government-backed programs offer favorable terms, lower down payments, and longer repayment periods, making them an attractive option. Understanding the various SBA programs and their specific requirements is essential for businesses looking to leverage these valuable resources.

SBA loans are not direct loans from the government; rather, they are loans provided by banks and other financial institutions that are partially guaranteed by the SBA. This guarantee reduces the risk for lenders, making them more willing to lend to small businesses. With the average interest rate at 7%, SBA loans often provide a more accessible and affordable pathway to capital.

Types of SBA Loan Programs and Eligibility

The SBA offers several distinct loan programs, each designed to meet different business needs. The most popular include the 7(a) loan program, the CDC/504 loan program, and microloans. Each program has specific eligibility criteria, loan limits, and uses for funds, so it’s critical to identify which one aligns best with your business objectives.

- SBA 7(a) Loans: The most common type, offering flexible financing for a wide range of business purposes, including working capital, equipment purchases, and real estate.

- SBA CDC/504 Loans: Designed for major fixed assets like real estate or machinery, promoting business growth and job creation.

- SBA Microloans: Smaller loans (up to $50,000) for startups and small businesses, often used for working capital or inventory.

Eligibility for SBA loans typically includes operating for profit, doing business in the U.S., having reasonable owner equity, and using alternative financial resources first. While the application process can be detailed, the benefits of these loans, such as competitive interest rates and longer terms, often outweigh the effort. Their role in facilitating small business growth remains significant, providing a vital pathway to capital in the 2026 financial landscape.

The continued importance of SBA loans and other government programs in 2026 underscores their role as essential tools for small businesses. By providing access to capital under more favorable conditions, these programs help mitigate the challenges posed by market interest rates, enabling businesses to invest in their future and contribute to economic growth.

Future Outlook: Trends and Predictions for Small Business Lending

Looking ahead, the future of small business lending in 2026 and beyond is expected to be characterized by continued innovation, increased digitalization, and a greater emphasis on data-driven decision-making. While the average 7% interest rate provides a current snapshot, evolving technological capabilities and changing borrower expectations will likely reshape how capital is accessed and distributed.

Fintech companies are poised to play an even more significant role, offering increasingly sophisticated and customized lending solutions. Artificial intelligence and machine learning will further enhance lenders’ ability to assess risk and process applications more efficiently, potentially leading to faster funding and more personalized loan products for small businesses. These advancements will create new opportunities but also new challenges in terms of data privacy and cybersecurity.

Emerging Technologies and Their Impact on Lending

The integration of emerging technologies is fundamentally altering the lending landscape. AI-powered underwriting, blockchain for secure transactions, and predictive analytics are all contributing to a more dynamic and responsive financial ecosystem. These technologies allow lenders to evaluate a broader range of data points, potentially expanding access to capital for businesses that might have been overlooked by traditional models.

- AI and Machine Learning: Enable faster and more accurate risk assessment, offering tailored loan products.

- Blockchain Technology: Enhances security and transparency in transactions, potentially reducing fraud and operational costs.

- Open Banking APIs: Facilitate seamless data sharing between financial institutions, allowing for a more holistic view of a business’s financial health.

These technological shifts are not merely about efficiency; they are about democratizing access to capital and making the lending process more transparent and accessible. Small businesses that embrace these digital tools and maintain robust digital financial records will be better positioned to capitalize on these advancements, ensuring quicker and more efficient access to funding.

The future outlook for small business lending in 2026 and beyond suggests a period of continuous transformation. Businesses that stay abreast of these technological trends and adapt their financial strategies accordingly will be best equipped to navigate the evolving market, secure competitive financing, and achieve sustained growth in an increasingly digital world.

| Key Point | Brief Description |

|---|---|

| Average Interest Rate | Small business loans in 2026 average around 7%, influenced by economic factors and lender risk assessment. |

| Diverse Financing Options | Includes traditional banks, online lenders, and government-backed programs, each with unique terms and eligibility. |

| SBA Loan Importance | SBA loans remain critical for providing accessible capital with favorable terms, reducing lender risk. |

| Future Trends | Lending will be shaped by AI, blockchain, and data analytics, leading to faster and more personalized funding solutions. |

Frequently Asked Questions About Small Business Lending in 2026

The average interest rate for small business loans in 2026 is projected to be around 7%. This rate can fluctuate based on economic conditions, the specific lender, loan type, and the borrower’s creditworthiness. Businesses should prepare for variations from this average.

To improve your chances, focus on maintaining a strong credit score, developing a solid business plan, having clear financial records, and demonstrating consistent cash flow. Providing collateral can also enhance your application and potentially lead to better terms.

Key types include traditional bank loans, online lender loans, Small Business Administration (SBA) loans (like 7(a) and 504), and microloans. Each offers different benefits and requirements, catering to various business needs and financial situations.

Yes, SBA loans remain an excellent option. They provide government-backed guarantees, which encourage lenders to offer more favorable terms, including lower interest rates and longer repayment periods, especially for businesses that might struggle with conventional financing.

Technology, particularly AI, machine learning, and blockchain, is set to revolutionize lending by enabling faster, more accurate risk assessments and personalized loan products. This will likely lead to more efficient and accessible funding options for small businesses.

Conclusion

Understanding the dynamics of small business lending in 2026, particularly with average interest rates hovering around 7%, is vital for any entrepreneur seeking to expand or stabilize their operations. The landscape is rich with diverse financing options, from traditional banks and online lenders to government-backed SBA programs, each offering unique advantages. By meticulously preparing financial documentation, maintaining strong credit, and strategically selecting the most appropriate funding source, businesses can effectively navigate this complex environment. The future promises further technological integration, which will continue to shape how capital is accessed, emphasizing the need for adaptability and informed decision-making. Ultimately, proactive engagement and a clear financial strategy will be the keys to securing the capital necessary for sustained growth and success in the evolving market.